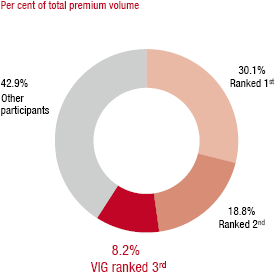

The three largest insurers in Poland hold a market share of 57%, and the remaining companies each have a market share of less than 8%.

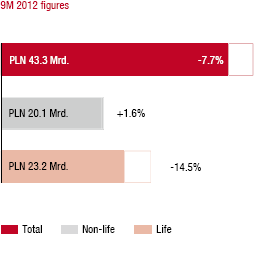

Insurance market premiums recorded a year-on-year drop of 7.7% in local currency terms in the 1st to 3rd quarters of 2013. This was due to a large drop of 14.5% in life insurance. Following strong growth in single-premium products in 2012, uncertainty about the statutory amendments taking effect in 2014 led to a massive decline in premiums in this area. The non-life segment, on the other hand, increased by 1.6%. The increase was due to non-life premiums excluding motor vehicle insurance, which grew by 10.9%. Increasing prosperity, with an accompanying increase in the demand for insurance, and a greater awareness of risk among the population contributed to this positive performance. Falling average premiums, on the other hand, had a negative effect on the motor vehicle business, which decreased by 5.8% in the 1st to 3rd quarters of 2013.

Insurance density was EUR 385 in Poland in 2012, of which EUR 161 was for non-life insurance and EUR 224 for life insurance.

Market growth in the 1st to 3rd quarters of 2013 compared to the previous year

Source: Financial Market Authority Poland |

Market shares of the major insurance groups

|

VIG companies in Poland

Vienna Insurance Group is represented by six companies and four different brands in Poland. The Group companies include Compensa Life and Non-life, InterRisk, Polisa and Benefia Life and Non-life. Compensa Non-life also has branches in Latvia and Lithuania.

VIG's total market share of 8.2% makes it the third largest insurance group in Poland. The most recent expansion took place in November 2013 with an agreement to acquire Skandia Poland.