VIG is an insurance company operating in the international arena. More than 50% of all Group premiums written in financial year 2013 were generated in markets outside of Austria. These markets vary greatly in terms of the maturity of their economies and insurance industries, and provide valuable diversification between reliable and high growth markets.

VIG's top priority in Austria is to consolidate its leading market position. In addition to maintaining existing customer relationships, growth potential also has to be actively exploited in Austria. For example, the country has a lower life insurance density than many other Western European countries. The Austrian VIG Group companies have on many occasions in the past demonstrated that they possess the know-how and experience needed to identify market trends at an early stage and successfully address them with innovative insurance solutions. They must continue to further develop these abilities in the future to ensure that Austria remains a stable foundation for the Group.

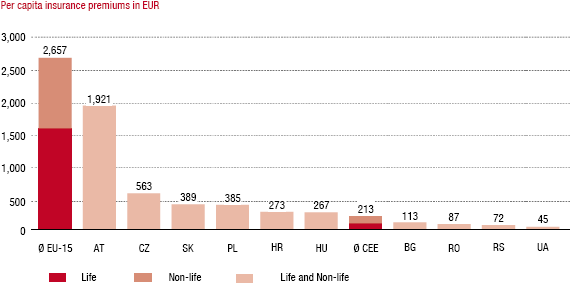

VIG's early involvement in the CEE markets, starting with its expansion into the former country of Czechoslovakia in 1990, give it a valuable head start. Since that time, it has acquired detailed knowledge of the special features and regional requirements of the different markets. Even though the beginning of the global economic and financial crisis in 2008 considerably reduced the speed of the economic convergence process in CEE markets, VIG remains convinced of the long-term potential of these markets. This conviction is supported, among other things, by a comparison of insurance density, which measures the average amount paid per capita for insurance premiums.

While VIG's core CEE markets had an average insurance density of EUR 213 in 2012, the comparable figure for the EU-15 countries was EUR 2,657. In the non-life insurance area, the comparison is EUR 112 to EUR 1,086. The potential is even greater for life insurance, which shows an insurance density of EUR 101 in core CEE markets and EUR 1,571 in the EU-15 countries. VIG Group companies provided impressive proof in financial year 2013 that they can also take advantage of this potential successfully. The VIG companies in Slovakia, for example, reported significant premium growth of close to 6% in 2013. Hungary even achieved growth of around 15% and Serbia almost 18%. The Baltic countries recorded a particularly satisfying increase of around 36%. We aim to continue these successes in coming years.

Insurance density 2012